As we continue to move towards a cashless society, kids need to be taught about money in a way that doesn’t rely on them actually seeing that money in front of them. This is why, as you’ll see from our Greenlight review, having a product like this that shows them how to responsibly use a debit card could be the solution.

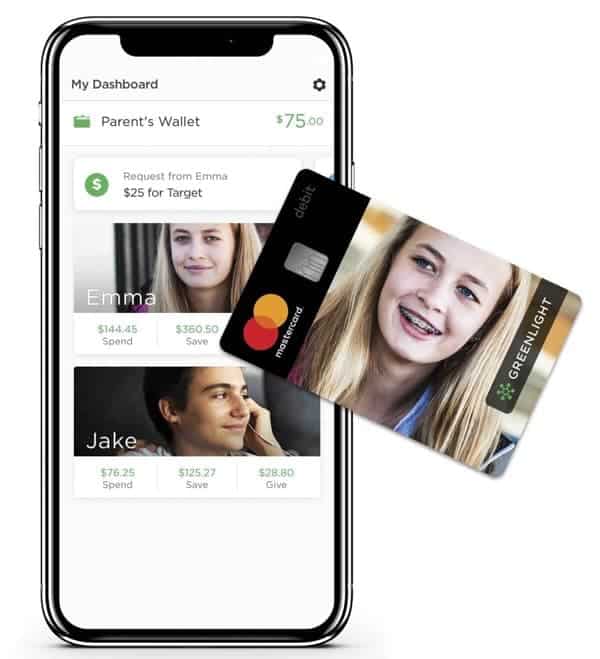

What Greenlight does is offer a debit card that’s just for kids, but that has full parental oversight. This means you’re able to see when, where and how much money your kids are spending to be able to guide them in the right direction.

But Greenlight has a ton more features than that to really help your kids understand how to manage their money properly – as well as to make the process easier for you.

And with more traditional money teaching methods, like putting coins in jam jars, not really being a realistic reflection of how we spend our money anymore, having a product like Greenlight could be just what you need to get your kids ready for spending in the digital age.

Why choose Greenlight?

• Great for teaching kids how to use debit cards responsibly

• Sick of remembering to pay your kids’ allowances? Greenlight can automatically transfer their allowance into their accounts each week

• Parents can add interest to encourage saving and even introduce kids to investing

• The monthly fee covers up to five kids – plus you get a one-month free trial

What is Greenlight?

Greenlight is a company that seeks to instill positive financial habits in children by offering a debit card that’s solely for kids but overseen by their parents. In doing so, kids are able to gain real-life experience in seeing the actual impact of their financial decisions.

Specifically, kids are able to spend using the Greenlight card while their parents monitor their purchases on the Greenlight app. There are also a bunch of other features that parents can add to their child’s account to further help them learn about effective money management.

How does Greenlight work?

Greenlight works much like any other debit card, except for the fact that it’s targeted at children and that their parents are able to monitor their spending activities. This means that children are able to make purchases using their card up to the amount of money contained in the account

However, parents can do more than simply see when, where and how much money their kids have spent through the Greenlight app. They can also:

- Immediately transfer money to their kids’ Greenlight card, including setting up regular, automatic payments for their allowance

- Receive a notification whenever a purchase is made with the card

- Set up payments for completed chores

- Set limits on stores where the card can’t be used, as well as ATM withdrawal limits

- Pay interest on their kids’ savings – a really great feature to encourage them to save more

- Deactivate the card through the app

You can see an example of what Greenlight’s chore management feature looks like below:

Kids can also have other features added to their Greenlight account, including:

- “Save the change”, allowing purchases to be rounded up to the nearest dollar with the difference then added to savings (like what Acorns does for adults)

- Set trackable savings goals

- Allow kids to track their own account in the special kids version of the Greenlight app (which they can still access through your phone if they’re not old enough for their own phone yet)

- Personalized debit cards (although these have an extra fee)

One other great aspect is the fact that all accounts actually have three “buckets”: the Spend, Save and Give buckets.

Kids can only spend money that’s in the Spend bucket and only their parents can move cash out of one bucket and into another. This also has other implications, like the fact that only money in the Save bucket will earn interest.

When combined together, it’s easy to see how all these features can have a huge impact on kids’ understanding of some key financial concepts.

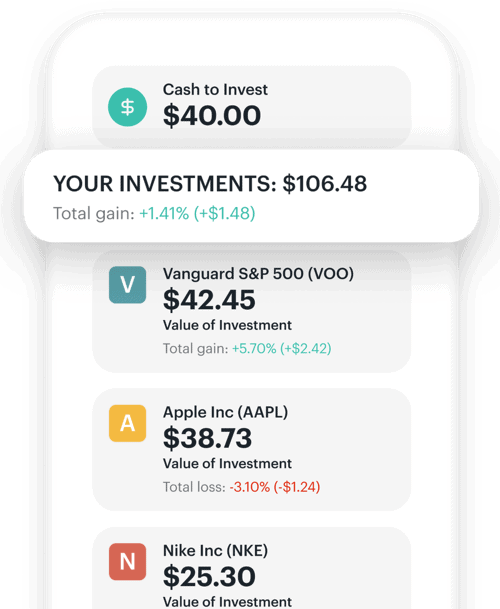

What’s Greenlight Max?

Greenlight Max is an upgraded plan that helps to teach kids how to invest. They’ll get all of the information they need to decide how they want to invest their money, with parents then having the final approval on any transactions.

As Greenlight themselves say, it’s important for kids to first learn how to save and budget their money between the three “buckets”. But once they’ve nailed that, teaching them the importance of investing – and the patience that comes with it – is going to be an invaluable lesson to ultimately set them up for financial freedom one day.

Does Greenlight charge a monthly fee?

After a one-month free trial, Greenlight’s plans start at $4.99 per month for the whole family, including up to five children. Their plans continue to upgrade from there, up to $9.98 per month for Greenlight Max, and you can cancel at any time.

Specifically, when it comes to how much is Greenlight a month, the different options include:

- Greenlight’s standard plan: $4.99 per month

- Greenlight + Invest: $7.98 per month

- Greenlight Max: $9.98 per month

Some other fees (and freebies!) to be aware of include:

- All ATM withdrawals are free (although ATM providers may add their own charges)

- Your first card replacement is free. After that, it costs $3.50 per card

- There are no foreign transaction fees if the card is used overseas

- If you want a custom card, there’s a one-off $9.99 fee

Advantages of Greenlight

Some of the highlights of Greenlight include:

- It’s a great product for teaching kids how to use a debit card responsibly. More traditional ways of teaching kids about money include putting cash in jars or similar strategies. But with society becoming increasingly cashless, it’s important to show children that swiping a card has actual financial implications too, which Greenlight does really well.

- The parent-imposed spending limitations are an excellent feature. It’s reassuring to know that kids can’t simply skip off into the sunset and spend their money how they want. By limiting where and how much money they can spend (in addition to Greenlight’s own restrictions), you’re helping them to learn about managing their finances in an age appropriate way.

- The fact that there’s a Greenlight app both for parents and kids allows your children to review their own money management. They don’t need to see everything you can see on your end, like the various limitations. Instead, they’re shown only what helps them on their financial journeys.

- Allowing parents to set the interest rate is better for motivating kids to save. Any interest offered in standard bank accounts is pretty negligible these days. By allowing you to set more significant interest rates, you’ll be motivating them to save more by letting them see the actual results of their savings.

- Teens with jobs can set up direct deposit so their paychecks are deposited in their Greenlight account. This helps ensure all their money is in one place, making it easier for them to manage.

Disadvantages of Greenlight

Some points you should keep in mind with Greenlight are:

- It’s really only for kids old enough to use a bank card. While there’s no Greenlight card minimum age, you may prefer your younger children to stick to cash for now – or to at least not have the freedom that this card offers. In those cases, something like FamZoo may be more appropriate.

- The only interest kids can earn is from their parents. While the fact that parents can set an interest rate (which, let’s be honest, is probably going to be higher than what any bank offers these days) is a great feature, it would be nice if there was some interest from Greenlight or its partner bank tied into this account too.

- The fees for using the investing features are quite steep when compared to returns. That is, your kids aren’t going to be investing thousands of dollars here, so when you consider that you’ll be paying between $2.99 and $4.99 more each month for being able to invest, that’s basically going to be their annual returns eaten up in a month. This means that a better option may be to invest their money in your much lower account – although you do then lose the relative autonomy they have (and the lessons involved) in learning how to do this themselves.

How do I add money to my Parent’s Wallet on Greenlight?

Money can only be added to your child’s account from the Parent’s Wallet. To add money to this, you can set up “Autofunding”, which automatically transfers money from your bank account when funds in your Parent’s Wallet reach a certain amount or on set dates. You can also “Add Money Now”. These are both done from the Parent Dashboard.

From there, you can choose to send money from your Parent’s Wallet to your child’s Greenlight card. This includes selecting whether you’d like to send the money to their Spend, Save or Give buckets.

For other ways to get some cash to your teens, check out these creative ways to give money to teenagers.

Is Greenlight legit?

Greenlight is definitely legit, with a rating of 4.2 out of 5 in the Google Play store from over 10,000 reviews and 4.8 out of 5 in the Apple Store from more than 143,000 reviews. It also has a rating of B from the Better Business Bureau.

There have been 37 Greenlight complaints on BBB, although the vast majority have been resolved, with Greenlight customer service having responded to each of them. This suggests that any complaints are being addressed.

When looking at any Greenlight reviews on Reddit, these are overwhelmingly positive. Most of them involve some discussion about Greenlight alternatives, including whether it would make more sense for their kids to just have a normal bank account.

These comments, however, seem to mainly be due to the lower fees charged on these accounts and the fact that their kids are older so can presumably handle an account with less parental oversight than Greenlight.

Is Greenlight FDIC insured?

Every Greenlight account is FDIC insured through Community Federal Savings Bank (CFSB). This means that if CFSB fails and certain requirements are met, your funds are insured up to $250,000.

To find out more on what this entails, check the FDIC site.

Why does Greenlight need my Social Security number?

Due to the USA Patriot Act of 2001, all financial institutions must verify the identity of all account holders. This is why Greenlight asks for information like your Social Security number, as well as other details like your birthday.

It’s worth noting that Greenlight’s Privacy Policy specifically states that your data will be held in full compliance with the Payment Card Industry – Data Security Standards. This includes personal information that was collected to verify your identity.

Is the Greenlight app safe?

The Greenlight app is safe in that there are a number of parental controls in place that can help protect your child while they learn to manage their money. Your Greenlight account is also FDIC insured, to ensure your money is protected.

Some of the main safety features include:

- Any data you upload to your Greenlight account, including photos of your child (which you can do when assigning an account to them), are encrypted.

- In addition to the spending restrictions parents can put in place, the Greenlight card can’t be used in places such as those offering wire transfers, adult entertainment, gambling and more.

- As it’s a debit card, kids can’t spend more money than what you give to them.

- Any direct deposits can only be from a child’s employer and in the child’s name, with any other transfers having to come from parents.

How does this compare to any Greenlight card alternatives?

There are several other companies with products that are aimed at helping kids learn about effective money management, including those that offer some great Greenlight alternatives.

We’ve got articles about each of these coming soon so once they’re available, we’ll link to them below:

- FamZoo vs Greenlight (and you can see our more detailed FamZoo review here!)

- Greenlight vs BusyKid (including an upcoming BusyKid review)

- Greenlight vs Current vs GoHenry (including whether Greenlight is better than Current!)

Final thoughts based on our Greenlight review

Teaching your kids how to responsibly use a debit card is definitely a lesson that will be useful for them almost every day of their lives going forward.

Whether or not this is the best debit card for kids in your opinion based on this Greenlight review will depend on what you need – as well as what you think your kids need.

That said, the level of parent oversight available is really impressive, and I’m a particular fan of the store-level restrictions you’re able to put in place. While kids do need to make their own mistakes to learn, having some limits like these are great for guiding kids in the right direction.

The main downside for most people will be if you’re looking for something that helps kids learn about money management but that doesn’t require them to have a debit card, especially if you don’t think they’re quite old enough for that yet.

If that sounds like you, one of the Greenlight card alternatives may be better. Otherwise, though, this is a really solid product that will put your kids ahead of even many adults when it comes to handling their finances.